An ancient Greek mathematician named Archimedes of Syracuse lived for roughly 75 years in the period between 287 – 212 BC. Considered one of the greatest mathematicians of all time, he studied and understood, among other things, the power of levers. Some of his inventions included the block and tackle pulley system where sailors could use leverage to lift objects that would otherwise have been too heavy to move.

Archimedes understood the power of applying the right pressure at the right place. He was so confident in ideas he said:

Give me a place to stand on, and I will move the Earth.

And while this could easily devolve into an article about financial leverage, that’s not the point.

The point is to get us thinking about how certain actions have a big impact on our lives.

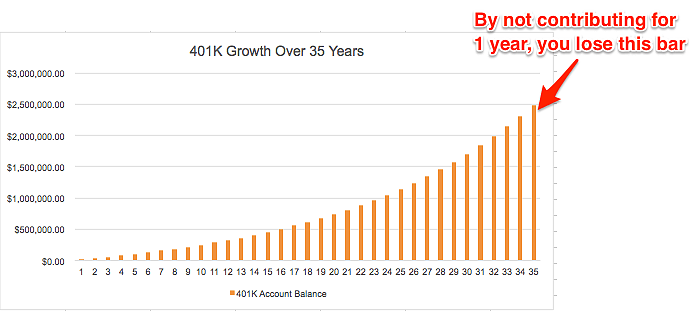

Deciding whether to start contributing to your 401(k) account when you start at the firm? It seems like such a minor decision, one that could easily be put off while you sort out competing financial constraints (security deposits, student loans, silverware), but one that has a profound impact on your ability to build wealth. As we’ve shown in previous graphics, skipping the 401(k) contribution even for one year means you’re giving up the profound growth on the right side of the chart. You may think you’re skipping out on $18,500, but it’s more likely that you’re cutting off hundreds of thousands of dollars from your eventual nest egg.

Or maybe you’re thinking about where to live. You could live in the cheap apartment close to work where you’ll be able to walk each day. Or you could get some more space by building in a little 30 minute commute. It may not seem like much at the time, but if you add 30 minutes to your commute, you’ve effectively created 15,660 minutes of wasted time each year (261 working days X 60 commuting minutes each day). That’s not to say that one path is better or worse for YOU, because we are indeed all special snowflakes, but I think everyone will admit that one seemingly innocuous decision can have a major impact on your quality of life.

Once you start to think of the world with a long time horizon in mind, you’ll start to value the smaller changes. Downgrade your Internet speed for a savings of $20 a month. You’ll notice no difference in your service and you’ll save $3,460 over a decade. That’s enough to pay for a new iPad ever 2.5 years, which you can now easily afford since you made a tiny change.

You’ll also start to appreciate the power of saving money. When I started, I didn’t find the Backdoor Roth IRA too convincing. It seemed like you had to jump through a lot of hoops (not true) in order to save $5,500. When you’re staring at $190,000 in student loans, saving $5,500 just doesn’t feel like it’s going to move the needle. It’s depressing and I get it because I was there.

But by that very argument, if $5,500 feels inconsequential, you won’t miss it when it’s gone. What’s $5,500 invested annually for 30 years at a 7% return? It’s $597,769. That’s a pretty significant amount of money that could generate $24,000 a year for you to live on using the 4% safe withdrawal rate. Or it could be a house. All because you started saving a small amount of extra money.

Yet, I know many of you will resist this idea. For whatever reason, humans aren’t built to understand the power of a series of small seemingly insignificant steps that lead to big changes. But yet we all understand levers, right? Given the right position, you can apply a little force and accomplish something previously impossible.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He spends 10 minutes a month on Empower keeping track of his money and is currently looking for additional lenders to add to Biglaw Investor’s JD Mortgage service which connects readers with lenders offering special mortgages for high-income professionals.

Really like this point you make about the effect of small actions. A lot of us don’t realize how tiny changes can add up over time. We all understand compound effects in theory, but in reality, it’s really hard to visualize.

About two years ago, I was sitting at my desk. I don’t remember exactly what I was doing – probably working on a brief or doing some research. What I do remember was that I was on my third Mountain Dew of the day. I wasn’t feeling great from it. And as I thought about it, I started thinking about how much soda I’d been drinking over the past few months and years. All that soda couldn’t be good for my health. So right then, I cut out soda completely.

It’s a tiny change. Just no more soda in my life. But the long term effects of it I’m positive will be big. It’s only been two years, but imagine the health benefits I’ll have from cutting out soda over the next 5 years, 10 years, 20 years, 30 years. It’ll add up. I just can’t really see it yet.

The same is true with tiny financial habits. Small changes, small savings, added up over a long period of time can lead to big results.

Thanks for sharing. I’d say cutting out soda from your diet is a pretty big change actually, but you’re right that it seems small and yet has a big impact on your life. Personally, I’m glad to hear that you’re human. With all the bike riding you do for your side gigs, I was beginning to think you might be the most “in shape” lawyer around. And maybe you are – you did mention this was three years ago!

Compounding interest is an incredible thing. Saving hundreds of thousands of dollars seems daunting until you look at the math and realize the advantage of starting early.

It’s also daunting in the beginning when you’re paying back loans and barely moving the needle. But consistency and hard work pays off. It’s been fun following your story on Mr Crazy Kicks.

Loved this– especially the chart! Its surprising what a difference even one year can make. And honestly you *might* have just convinced me that we need to start funding our retirement, even if it is only at $5500 per year. For some reason, seeing it calculated out at almost $600k is really motivating (except that is also almost exactly how much we have in student loans). We go back and forth all the time on whether to throw everything at our loans or start funding retirement.

Hey Amber, thanks for leaving the comment. I stopped by your site and read about your situation. When I started out, I owed $190K in student loans (so if there had been two of me, it would have been $380K). Initially I threw everything at my loans to the detriment of retirement savings. It was just THAT important for me to get out of debt. In hindsight, I might have been a little too focused on reducing the debt. Contributions to retirement accounts, particularly when you have a high income, do a lot to reduce the tax drag on building wealth since you’ll be saving taxes at your marginal rate today and paying them at your effective rate down the road (likely to be much lower and if not, that’s a good problem to have). Even in your situation, I would consider starting the 401(k) contributions.

You might also like:

https://www.biglawinvestor.com/contribute-401k-or-pay-off-student-loans/

https://www.biglawinvestor.com/the-dreaded-401k-penalty-clause/

Looking forward to following your blog.

Thank you for this response! I’m checking out your other posts now.

Could you explain the math behind “What’s $5,500 invested for 30 years at a 7% return? It’s $597,769” as far as I can tell that’s $5,500*(1.07)^30 = $41,867.40. What am I not seeing?

$5,500 invested every year for 30 years at a 7% return. I edited the post to make that point clearer.

Thanks for the clarification. Excellent post.

Show me an investment vehicle that WILL dependably return 7% every year, for the next 30 years. This was once the case with index funds…barely. However, I don’t see that being possible without some pretty savvy management going forward…and you didn’t calculate the fees associated with having that money ‘managed.’ You’re not presenting a realistic and ‘whole story’ approach to this model.

Even if it’s 5% real returns, it’s $400,397 in a Roth IRA ($304,575 in taxable). 4% is $336,433. Still substantial returns in 30 years for what might equate to 2-3% of a high-income professional’s salary.