In retirement planning, the concept of the 4% safe withdrawal rate is a well-known metric for the approximate percentage of a portfolio you can withdraw over a 30-year horizon with the expectation that the portfolio will still be there at the end of the 30 years.

It’s based on a study of three finance professors from Trinity University (San Antonio, not Dublin) where they recorded the effects of a range of nominal and inflation-adjusted withdrawal rates applied monthly on the success rates of retirement portfolios of large-cap stocks and corporate bonds for payout periods of 15, 20, 25, and 30 years. They updated the study in 2009.

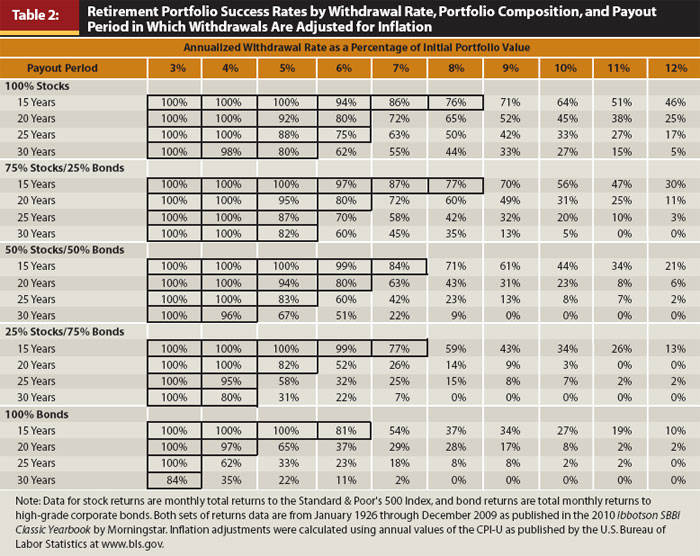

In other words, they looked at hundreds of historical 30-year periods and measured the success rate of different withdrawal rates on different equity/bond allocations.

When looking at 30-year periods from 1926 to 2009, they found that a 75%/25% allocation between stocks and bonds produced a 100% success rate with inflation adjusted monthly withdrawals at 4%.

This is the most important chart from the study.

Source: Portfolio Success Rates: Where to Draw The Line

That means you could withdraw 4% of the initial portfolio balance each year, adjusted upward for inflation, with a 100% success rate for a portfolio divided between equities and bonds at 75%/25% .

Example 1. Larry has a $1 million portfolio in 1952. He withdraws $40,000 in year 1, $40,760 in year 2, $41,045 in year 3, etc. increasing with inflation (the early 1950s were a low time for inflation). He has a constant stream of $40,000, adjusted for inflation, at least until 1982.

Despite the popularity of this study, surprisingly the 4% safe withdrawal rate not well-known outside of retirement planning circles.

Problems with the 4% safe withdrawal rate

There are a few important considerations to keep in mind when relying on the 4% safe withdrawal rate.

- Thirty (30) year periods. The study measured retirement periods of thirty years. That will take a 65-year-old through the age of 95. But what about people retiring earlier? If you’re a lawyer that plans on stopping work at age 55, can you rely on the study for a retirement that could stretch 40 years? Also, as people are living longer and longer, do you want to take a risk that your money could run out in your mid-90s during a state of life where you won’t be able to work? The validity of the Trinity Study is highly debated in early retirement circles where people are planning on living on money for 50 and even 60 year stretches.

- Portfolio Success. Tying into the point above, the Trinity Study considered the portfolio to be a success if on the last day the portfolio had zero or greater dollars. In other words, you could drain the portfolio down to the bottom on the 364th day of the 29th year and the study deemed the portfolio successful. If you’re a little concerned about getting that close to the bottom, you might be skeptical of the 4% withdrawal rate.

- Past Data. All the analysis is based on past data. Nobody knows how the market will perform in the future. Understand that this undermines the people who argue that the Safe Withdrawal Rate should be higher or lower too.

- Low Rate. A 4% withdrawal rate doesn’t seem that extreme when you realize that you could withdraw 3.33% annually of a portfolio consisting entirely of cash and expect it to last 30 years (X/30 = 3.33%). Granted, this would be using nominal dollars which would result in a important decrease in your standard of living over the 30-year time horizon, but the 4% withdrawal rate is a fairly conservative number (i.e. that’s why they call it the safe withdrawal rate). In many of the 30-year periods, a 4% withdrawal rate resulted in a significantly higher portfolio balance at the end of the 30-year periods. You could very easily end up with more money than you started!

There’s also a bunch of articles that are pessimistic about future equity performance and recommend moving the safe withdrawal rate to a lower number (usually 3%). There’s something about the safe withdrawal rate that attracts people who love to play with numbers. EarlyRetirementNow is putting on a tour de force of technical calculations on the fallacy of the 4% safe withdrawal rate. If you’re interested, I highly recommend reading through his excellent series. You’ll learn a lot about the 4% withdrawal rate and why it’s ridiculous to approach it dogmatically with the expectation that you’ll be able to withdraw 4% each year. I’m not sure where he’s going to land on a true “safe withdrawal rate” but presumably it will be much lower than 4%. Ironically, his article has reinforced my belief that the 4% number is fine for planning purposes.

How to use the 4% safe withdrawal rate

First, you should understand that the math behind the rule makes it very simple. All you need to know to figure out your “number” is take the amount of income you would need to cover your current living expenses and multiply it by 25.

Example 2. Larry makes $50,000 a year. He pays $10,000 in taxes and lives on $40,000. He needs approximately $1,250,000($50,000 x 25) to retire.

If you’re like most people, that number might seem a lot lower than you thought it would be. Can you really retire on $1.25 million?

To others, you might be thinking that $40,000 is an impossibly small amount to live on in retirement. The truth is that every study I’ve read shows that overall expenses go down in retirement. Sure, you may travel the world for a couple of years or buy a boat, but you can only keep that spending going for so long. After taking three international trips a year for five years, you might start to prefer hanging around the house. We also know that when you have more time, your spending is likely to decrease as you rely less and less on paying higher prices for convenience items (pre-made meals, cleaning services, etc.).

Second, you should keep in mind that the 4% safe withdrawal rate is just a guide. No retiree in their right mind is going to calculate 4% of the initial portfolio amount and withdraw it consistently (adjusting upward for inflation) each year. Without fail, every actually old retired person I’ve spoken to has told me that some years you withdraw a little more when the market is good and some years you withdraw very little when the market is bad.

Here’s a great takedown on the Bogleheads about the complexity vs simplicity when it comes to SWR. The biggest criticism is that the poster retired at the beginning of a great bull market and was therefore able to withdraw much more than 4% in retirement. But it’s insane to me when people make calculations assuming a 1995 retiree would have kept on spending through 2007-2010 as if everything was fine. People are not automatons!

Which means, if Larry from the example above has $40K in fixed expenses each year that he cannot change, retirement is going to be a little more dicey. If he has $20K in fixed expenses but another $20K in variable spending, he’ll have the flexibility he needs to get through the rough patches.

I could write about a host of other reasons why the pessimists shouldn’t carry the day on calculating retirement spending (perhaps a subject for a future post). Calculating 25 times the income needed to cover your current annual expenses is a perfectly reasonable starting point for figuring out your number. Once you calculate your reasonable expenses in retirement, your “number” might be a lot lower than you think.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He convinces the student loan refinancing companies to give you cashback bonuses for refinancing your student loans and looks forward to you discovering how easy it is to track your net worth with a free tool like Empower.