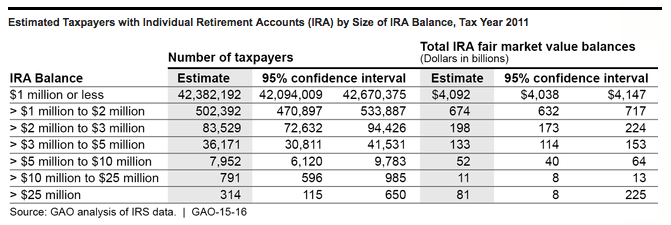

The government keeps detailed statistics on its citizens, some of which make headlines but most of which go unnoticed. One statistic recently caught my attention and particularly the number 314.

Why 314? Because there are at least 314 people with Individual Retirement Accounts with balances over $25,000,000. Let that sink in for a moment.

Over 314 people have IRAs with more than $25 million dollars.

You might be asking yourself how someone could have a $25,000,000 IRA when the contribution limits amount to only $275,000 during an average career? Even the more generous contributions under the SEP-IRA can’t explain balances of this size.

Yet, the numbers don’t lie:

And yet according to the government numbers, these accounts exist.

Real life examples of multi-million $$ IRAs

One case study we can look at is Peter Thiel. You may know him as the venture capitalist billionaire co-founder of Paypal. Or you may have read about how he funded Hulk Hogan’s lawsuit against Gawker. Either way, you probably didn’t know that he is a personal finance genius.

It’s rumored that Peter Thiel, one of the early investors in Facebook, partially funded his investment in Facebook through his Roth IRA. If he put as little as $100,000 into Facebook back in 2004, he could easily have over $25,000,000 in a Roth IRA account by now.

Notice that the government statistics don’t reveal whether the IRAs in question are traditional IRAs or Roth IRAs. I imagine that most of them are traditional IRAs with pre-tax money, if only because you can contribute over $50,000 to a SEP-IRA which makes the high balances more likely.

However, I’m most intrigued at the thought of these megabalances being held in a Roth IRA. If you’re reading this blog and don’t know the tax benefits of Roth IRAs, then I have failed you, but it’s worth a quick recap: you invest with after-tax dollars but the money grows tax-free and is withdrawn tax-free. That means if you have a Roth IRA account with a balance over $25,000,000, all of that money is yours to keep. No more taxes. Talk about a smart investing move, right?

Self-directed IRA

The trick to using your Roth IRA wrapper to invest in alternative investments like real estate, private company stock and intellectual property is to establish a self-directed IRA. Technically speaking, a self-directed IRA is not any different from any other IRA. It’s just that self-directed IRAs have a wider range of available investment options.

Self-directed IRAs have been around since the IRA was created in 1974, but don’t receive the same level of attention as other IRAs because most custodians who offer IRAs (like Vanguard) only allow traditional investments at their firms.

There are some limitations to what you can and can’t do with an IRA. For instance, here’s a list of the basic prohibited transactions:

- You can’t buy or sell property directly from yourself.

- You can’t lend money or borrow money from it.

- You can’t invest in a company you own or control.

- You can’t do business with a company you own or control (e.g. if you have a rental property in your IRA, you can’t have the rental property hire your landscaping company to trim the lawn).

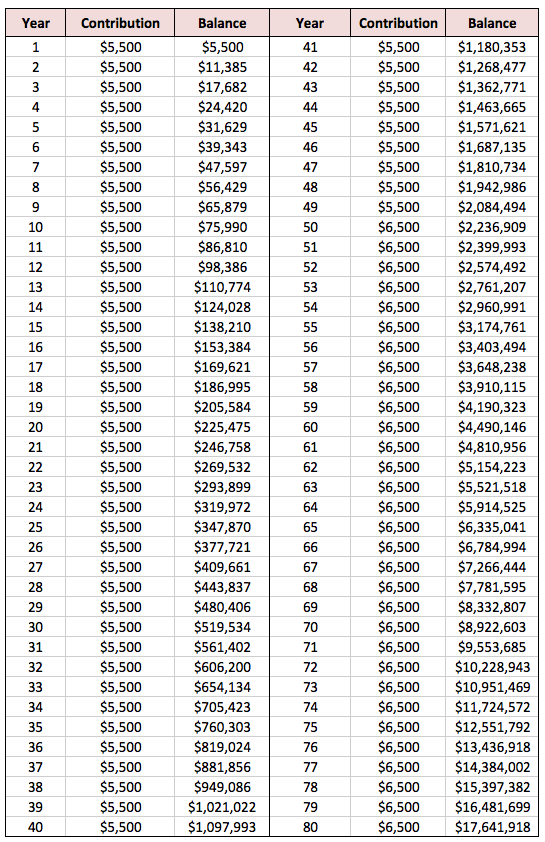

How to build a $100m Roth IRA

Another famously large IRA balance belongs to Mitt Romney, who purportedly holds over $100,000,000 of his wealth in an IRA. He’s never publicly revealed what investment are inside his IRA, but here’s my best guess.

Mitt Romney is a private equity guy. That means he makes most of his money through carried interest. Carried interest is a tax loophole that everyone promises to close, but nobody does.

Carried interest works like this: a private equity firm finds a company to purchase, say for $100M. Its limited partners put up $99M for the purchase, meanwhile the private equity firm adds the remaining $1M. In exchange for the $1M, the private equity firm enters into an arrangement with the investors where the private equity firm will take 20% of any profits achieved on the sale of the company.

Five years later, the Company is sold for $300M. After returning the original equity to the partners, the private equity firm is left with a $200M profit. Forty million goes to the private equity firm and the remaining $160M is distributed to the limited partners as profits.

The private equity firm may divide up the profit by only a few people. Let’s say it has four partners. Each will get $10M from the sale. If you assumed each paid ordinary income tax on the $10M profit, you’d be mistaken. Instead, they pay capital gains tax rates on their “carried interest” (the 20% cut of any profits).

If Mitt Romney used his IRA to make an investment in the carry vehicle of the private equity fund, any profits he received from the carried interest would fall into the IRA. He could then use the larger balance in the IRA to make more investments in future deals. I imagine this is how he built up such a large IRA balance.

How can you use this strategy?

Most lawyers should be focused on maximizing their retirement accounts and investing in index funds. The surest path to wealth is consistently saving money and getting market returns, which is what I’m currently doing.

But, if you have access to investment opportunities in private companies, it’s worth considering whether your Roth IRA is the right vehicle for such an investment.

Let’s consider an example. A friend of yours has started a niche manufacturing business selling a seasonal product. He has the product manufactured in China, imports it into the United States and then sells it at retail stores and through his own website. He’s looking for investment capital from you of $25,000 to help grow the business in exchange for a 1% ownership stake in the company.

If you think the company is doing well and likely to make a profit, you can make the investment from your taxable account. Any dividends or gains will be taxed at capital gain rates, which are more favorable than ordinary income tax rates but can still be quite steep once you factor in the 3.8% tax for Obamacare and state tax rates for capital gains (usually ordinary income tax).

If you think the company is doing well and likely to make a profit, you can make the investment from your taxable account. Any dividends or gains will be taxed at capital gain rates, which are more favorable than ordinary income tax rates but can still be quite steep once you factor in the 3.8% tax for Obamacare and state tax rates for capital gains (usually ordinary income tax).

On the other hand, if you make the investment through your Roth IRA, all dividends and gains will come back to you tax free. Keep in mind that if the company goes bust, you’ll lose everything and won’t be able to contribute the money back into your Roth IRA. This makes it risky since contributions to a Roth IRA can only be made once. However, the upside is also intriguing since you can avoid a large amount of taxes on a investment that does well.

Clearly Peter Thiel and Mitt Romney believed in their investments enough to make them with tax-sheltered money. So, the thing to consider is whether you should put your moonshot investments in a Roth IRA. As far as I can tell, if you’re going to make a risky investment, it’s a reasonable place to consider.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He spends 10 minutes a month on Empower keeping track of his money. He’s also maxing out tax-advantaged accounts like 529 Plans to minimize his taxable income.