Prioritizing investments is more art than science. The decisions are highly personal. Some people hate debt. Others have strong feelings about future tax rates. To serve as a talking point, I’ll lay out my view of the proper prioritization of investments.

If you’re a high-income earner, prioritization is less of an issue. You should be maxing out all retirement accounts (as I’m doing). But I recognize that even new lawyers with high incomes need a starting point.

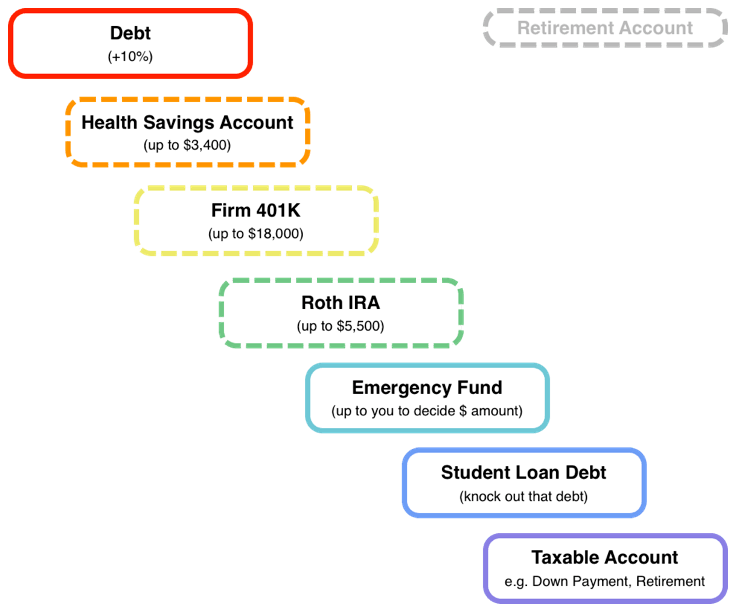

The following waterfall should work well for many lawyers:

1. Pay Off High Interest Debt. This is obvious and not worth much discussion. If you brought any credit card debt or other high-interest (above 10%) debt to your professional life, you need to eliminate it immediately.

2. Health Savings Account (HSA). If available to you (i.e. you are participating in a high deductible health insurance program), the HSA is a triple-tax-advantaged account with no income restrictions (sometimes referred to as the Stealth IRA).

3. Firm’s 401K Account. If you get a match, this should be your top priority, however most firms in my experience do not provide a match. Much has been written about whether to invest through a Traditional 401K or a Roth 401K. My opinion is to stick with the Traditional 401K and take advantage of the tax savings today.

4. Roth IRA. If your income is above $132,000 ($194,000 married filing jointly), you won’t be able to contribute directly to a Roth IRA. However, Congress has kept open the “backdoor” which allows you contribute to a non-deductible IRA and then roll it over to a Roth IRA. Roth IRAs act as great “emergency funds” because, if you absolutely had to, you can withdraw contributions at anytime without paying any taxes or fees. I wrote a Backdoor Roth IRA guide to show you how to do it step by step.

5. Emergency Fund. In the past, I’ve argued that you really don’t need an emergency fund in the traditional sense. However, it would be silly not to build up savings that can carry you if you need to leave your current job. If you have taxable investments, you can always sell some of those to cover living expenses in the event of a job loss, so you don’t have to keep this money in cash under the mattress. I have six months of expenses invested in a 60/40 mix of bonds and stocks which also fits into my overall asset allocation per my Investment Policy Statement. There’s a substantial peace of mind benefit to knowing that you could leave your current job and live for many months while you found a new gig.

6. Pay off Student Loan Debt. Student loan debt, even of the low interest kind, is not something wealthy people let linger (student loan refinancing only gets you so far; you still have to do the work and make the payments). Better to knock out the debt and stop paying interest to your lender than to effectively invest on margin with the hope of arbitraging the rate of return between your student loans and returns in the market. I can see in some cases where lawyers managed to lock in interest rates below inflation (i.e. 1.5% or 2%) where it might not make sense to pay off the debt. Still, consider that by paying off the debt you will significantly improve your cash flow position which allows for more choices in life and your career.

7. Car Savings Fund. Living in NYC, I don’t own a car. That may change in the future and when I do, I’ll be paying for it in cash.

8. Down Payment Savings Fund. If you’re thinking about buying a condo or house in the near future, it’s helpful to earmark a specific account or line item in your net worth calculation to keep track of this money.

9. Taxable Investment Account. If you still have money left over, now is the time to start piling it into a normal taxable investment account (in low-fee index funds obviously). This should only be after taking full advantage of all retirement accounts.

Two accounts I didn’t mention are: (1) 529 accounts and (2) the Mega Backdoor Roth.

529 accounts are state-specific investment accounts for education savings. They are a good deal but only worth it if you have kids (which I don’t yet). The Mega Backdoor Roth IRA probably isn’t available to you, but worth looking into just in case.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He spends 10 minutes a month on Empower keeping track of his money. He’s also maxing out tax-advantaged accounts like 529 Plans to minimize his taxable income.