Like most lawyers, you probably started with a negative net worth. It may seem like it takes forever to pay off the debt and accumulate your first $100K of assets. I remember how that feels and put together this post to remind you that the first $100K is the hardest.

Like a rocket hovering for a few seconds after liftoff

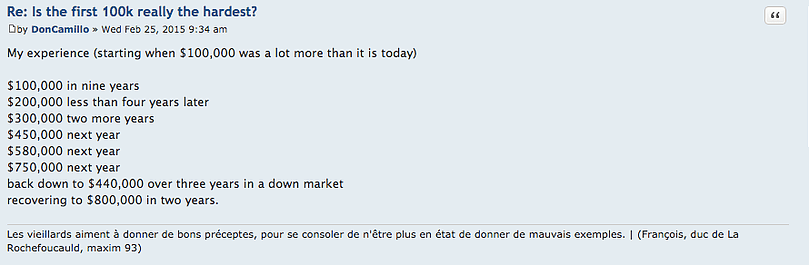

A few days ago I was reading a post on Bogleheads about saving your first $100,000. I bookmarked that discussion a long time ago and refer back to it from time to time. I find it inspirational to look at the progress of people saving and building wealth.

One of the best posts highlights how it took the poster nine years to save the first $100,000. For a lawyer with $250,000 in student loan debt, getting to a positive net worth of $100,000 is going to take some time, although I hope you can do it in less time.

But once the ball gets rolling, the compound interest starts to make a big difference. By the time the poster had saved $450,000 it only took one additional year to jump up to $580,000. Now that’s progress!

Why saving gets easier over time

Brute Force. While most of saving is done through brute force, this is especially true at the beginning and when you’re paying off student loan debt. Brute force is the only tool in your arsenal. Want $100K? You have to save basically every one of those dollars. Investments aren’t going to carry the way.

Startup Expenses. Life is expensive when you’re just starting out. New apartment? You might need some furniture. Professional wardrobe? You didn’t have that in law school. The list goes on and on. It’s not cheap to get established and some of those expenses are not optional.

Salary Increases. Whether you start in Biglaw, a smaller firm or public interest, your starting salary is significantly lower than the money you’ll be making once you gain more experience. It’s no surprise that it’s easier to save money on a high income than it is on a low income. My advice is to set up a system so that any amounts in excess of $X are sent to an investment account. It’s up to you to decide what $X will be, but a system like this is effective in letting you bank your raises.

Compound Interest. $100,000 will earn $10K at a 10% return. $500,000 will earn $25,000 at a 5% return. At a certain point, your investment returns make a greater contribution to savings than you can through brute force. Obviously that takes time.

Inflation. Inflation devalues the dollar. The second $100,000 is worth less than the first $100,000 unless you’re in a deflationary environment.

Paid Off Debt. As you’re saving now, a significant chunk of each month’s payment goes to servicing the loans. Once you’re debt free, you’ll no longer have that problem. A young lawyer with $200,000 in student loan debt could easily be paying $1,000 a month in interest alone (or less if they followed the Student Loan Refinancing Guide) and is probably paying a significant amount more.

Every Dollar Counts. Too proud to sign up for a program like Ebates that gives you cash back when you shop online? That’s too bad, because those dollars add up over time. I’m looking for $1 million of them and Ebates has paid me over $500 for just doing what I was going to do anyways. I love the easy wins!

Actually, the first million is the hardest

Unfortunately, while the first $100K is significant because represents getting out of debt and achieving a substantial positive net worth, there’s still more saving to do.

And the sad news is that it’s going to take a lot of brute savings to get to the $1M mark. Thirty precent of returns on a $300K portfolio is only going to get you closer to $400K. You’ll still need to be making substantial contributions to your nest egg. In fact, there’s a similar thread on moving the net worth needle from $1M to $2M.

T. Boone Pickens

Not to be outdone, I’m reminded of this famous twitter exchange between Drake and T. Boone Pickens that actually happened in 2012. Classic.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He convinces the student loan refinancing companies to give you cashback bonuses for refinancing your student loans and looks forward to you discovering how easy it is to track your net worth with a free tool like Empower.