Capital gains can mean increased state and federal income tax payments for taxpayers. But if you’re thinking of selling some of your capital assets, there are a few things you should know.

For example, let’s say you’re moving from NYC to California. You want to sell a significant chunk of equities to come up with 20% down for a condo purchase in California. The question is: Is it better to sell the equities in New York before you move? Or wait until you’re in California?

It turns out the answer is clear: sell in New York! You’ll pay a higher rate for capital gains if you wait, which means it can cost extra money to sell your stock after establishing residency in California.

I don’t usually give much thought to state capital gains tax rates. For the most part, I’ve minimized all capital gains taxes by sheltering them in tax-protected accounts (like an IRA retirement account) or by taking advantage of tax-loss harvesting to manage capital losses and offset gains.

However, I think this is a common enough example of when you might pay a higher tax fee that it’s worth exploring in more detail.

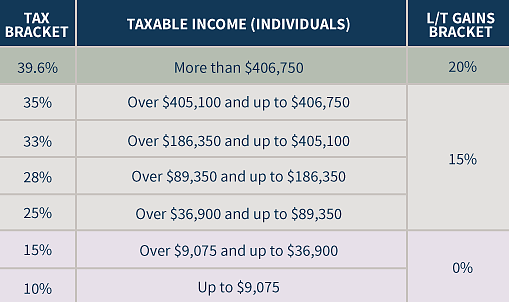

Federal capital gains tax rate

Most investors are aware of federal capital gains tax rates. Short-term capital gains are taxed at your marginal income tax rate. Long-term capital gains are taxed at either 0%, 15%, or 20%.

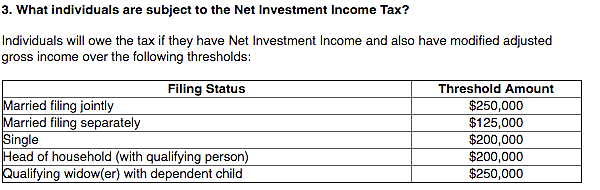

However, tax law requires an additional 3.8% Net Investment Income tax on unearned income. It’s to fund the Affordable Care Act and is only for certain income levels, according to the Internal Revenue Service (IRS) website.

State capital gains tax rate

A few states (California, New York, Oregon, Minnesota, New Jersey, and Vermont) have higher income tax rates—so it makes sense they have high taxes on capital gains, too.

In our example using California and New York, state capital gains are taxed at your ordinary income tax rate. There is no special tax rate for capital gains income. That’s largely a federal tax invention.

This means significant differences exist at the state level in “state capital gains tax rates.”

As is the case with federal capital gains tax rates, fluctuations in your taxable income can impact your final tax rate. For example, if you’re taking some time off between moves and jobs, your income will likely be lower that year.

Since lower income can result in a lower rate for taxes, it’s a great year to incur capital gains (assuming you planned on incurring them all along).

In fact, if you’re taking some time off, you should consider what other tax options might be available to you. Consult with an excellent tax accountant to see what your options are—some people are taking nearly $100,000 of investment income and not paying any taxes.

As with all things related to tax, a little planning goes a long way.

A hypothetical – married couple with $300,000 of personal income

To calculate the potential benefit or disadvantage of incurring capital gains in New York or California, let’s use the following facts in our hypothetical:

- Married Couple

- Married filing jointly tax return filing status

- Combined adjusted gross income of $300,000

- Sale of equities resulting in $50,000 of capital gains

Capital gains tax rate California

In California, they would pay the following tax on the $50,000 of capital gains:

- Federal capital gains tax: ($50,000 X 0.15) = $7,500

- Affordable Care Act tax: ($50,000 X 0.038) = $1,900

- California state tax: ($5,100 X 0.1038) + ($44,900 X 0.1138) = $5,639

- Total tax due: $15,039

- Effective capital gains tax rate: 30.08%

Capital gains tax rate New York

In New York, they would pay the following tax on the $50,000 of capital gains:

- Federal capital gains tax: ($50,000 X 0.15) = $7,500

- Affordable Care Act tax: ($50,000 X 0.038) = $1,900

- New York state tax: ($50,000 X 0.0685) = $3,425

- New York local tax: ($50,000 X 0.03648) = $1,824

- Total tax due: $14,649

- Effective capital gains tax rate: 29.30%

- Extra taxes paid by selling in California: $389

So, you could have an extra $389 in tax liability by selling the equities in California. That’s not too bad, but it would be worse if the capital gains are larger than $50,000 (which it might be, depending on your real estate market and how much you sell for a down payment).

This is because the California tax system taxes income at 11.30% up to $508,500 and then at 12.30% above $1,000,000. New York (including the NYC tax) taxes income at 10.50% up to $500,000 and then at 10.73% up to $1,000,000.

If your combined income is higher than $500,000 and your capital gains are above $50,000, the tax difference may run into the $1,000s. I think it’s safe to say that a little tax planning in this area is easily worth your time.

What about states with no income taxes?

Not every state has income taxes. So, would the outcome be different if you moved to a state with no income tax (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming)?

As you’ll see from the calculations, a high-income earner moving to Texas or Florida would benefit greatly from waiting to sell any capital gains used for a down payment.

- Federal capital gains tax: ($50,000 X 0.15) = $7,500

- Affordable Care Act tax: ($50,000 X 0.038) = $1,900

- State tax: ($50,000 X 0) = $0

- Total tax due: $9,400

- Effective capital gains tax rate: 18.80%

- Extra taxes paid by selling in California: $5,639

I don’t know about you, but an extra savings of $5,639 seems like a significant amount of money to me.

Finding a great financial advisor can help you keep the most money in your pocket when making decisions like this. But if you want to see for yourself, here is a great calculator for estimating capital gains taxes.

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He knows that the Bogleheads forum is a great resource for tax questions and is always looking for honest advisors that provide good advice for a fair price.