Many lawyers understand that taxes are their biggest expense each year and are looking for ways to shave their tax liability and lower their tax bracket. One of the best retirement accounts available is the Roth IRA.

High-income earners can contribute to the Backdoor Roth IRA, which is a simple two-step process for getting an annual contribution of $6,000 into a Roth IRA, even if you are over the income limit.

Contributing $6,000 every year for the next 30 years to your retirement savings, you could end up with a beautiful side account worth $512,000+

Are you considering a strategy to invest taxes into a Backdoor Roth IRA? Here is a comprehensive step-by-step guide for popular reference.

What is a backdoor Roth IRA?

A Roth IRA is an individual retirement account (IRA) containing investments with tax benefits like tax-free growth and qualified tax-free distribution or withdrawal (extenuating exemptions also available).

A traditional IRA offers tax-deferred growth, but a Roth IRA gives you tax-free distributions in retirement.

Here’s how that works: You pay taxes on the amounts contributed to a Roth IRA today in exchange for not having to pay taxes in the future. Roth IRAs are a great strategy for ensuring you have access to before-tax and after-tax dollars in retirement.

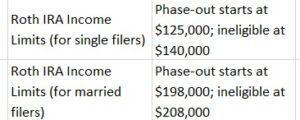

Congress has limited those who can contribute to a Roth IRA to taxpayers who earn below $140,000 for single filers and $208,000 for married filing jointly (subject to annual variations). Unfortunately, these eligibility income limits exclude most lawyers from being able to contribute.

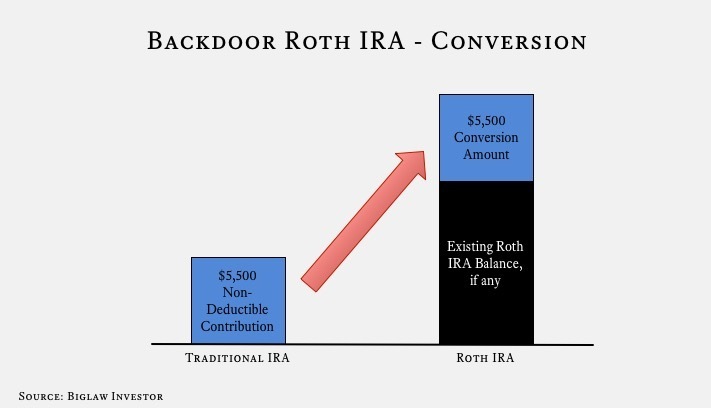

But there’s a catch: Since 2010, the government allows anyone, regardless of income, to convert a Traditional IRA to a Roth IRA by paying income tax on any account balance being converted that has not already been taxed.

Therefore, you make a Traditional IRA contribution of $6000 (the contribution limit as of 2021) each year. Because your income is likely too high to allow for this contribution to be tax-deductible, your contribution is known as a non-deductible IRA contribution.

It’s “non-deductible” in the sense that you can’t take a tax deduction on the contribution on this year’s tax return and therefore must pay income taxes. However, no matter your gross income, anyone can make a “non-deductible” contribution to a Traditional IRA up to that year’s limit.

From there, you simply convert the “non-deductible” contribution from a Traditional IRA to a Roth IRA. Because you already paid taxes on the “non-deductible” contribution to the Traditional IRA, there are no taxes to pay on the conversion.

Regardless of your income, anyone can convert money in their Traditional IRA to their Roth IRA, hence the “backdoor” two-step process of getting money into a Roth IRA if your income is too high to make a direct “front door” contribution.

The end process leaves you with a $6,000 contribution to your Roth IRA.

Does the IRS approve of the backdoor Roth IRA conversion?

I’m not aware of any situation where the IRS has reversed a Backdoor Roth IRA. If you know of one, please let me know. I’ve also never seen a tax court case resolving the matter one way or another.

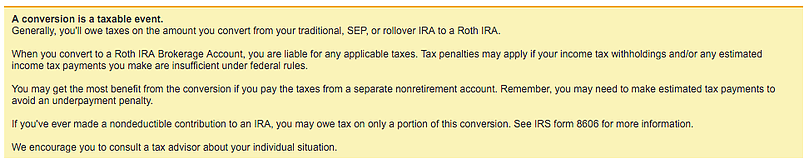

It’s clear that everyone, from Congress to the IRS to the financial institutions, is aware of the Backdoor Roth IRA. Just look at the ads from Charles Schwab and Fidelity:

In fact, Vanguard even mentions the backdoor conversion on its site.

If the IRS or a tax court invalidates Backdoor Roth IRA contributions, we’d have quite a mess on our hands. However, if you have questions or are unsure whether it’s the right step for you, check with a tax professional or financial advisor to discuss any potential tax consequences.

Do I need to contribute via the backdoor?

If you make less than $140,000 as a single person (or $208,000 for married couples filing jointly), you fall within the Roth IRA income limits. In that case, there is no reason to use the “backdoor” because you can make a regular contribution to a Roth IRA.

If your income is above these amounts, you should contribute to a Backdoor Roth IRA.

How to make a backdoor Roth IRA contribution

Let’s get started. My favorite platform is Vanguard, and it’s what I recommend.

Each step below tells you what to do and how to make a Vanguard Backdoor Roth IRA contribution.

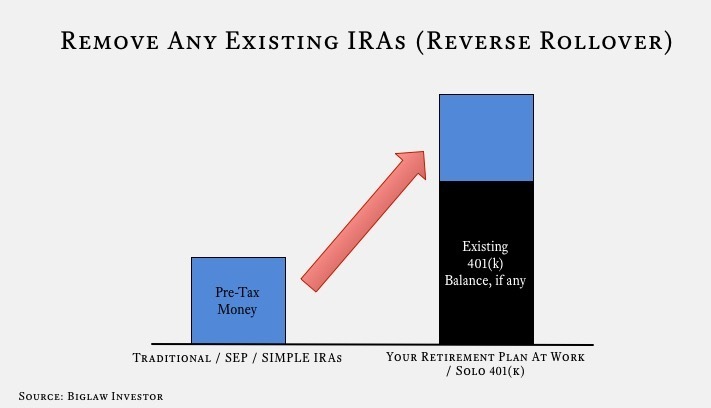

STEP 1) Convert/Remove “other” IRAs

If you don’t have any Traditional, SEP or SIMPLE IRAs with pre-tax money, go directly to step 2. You might have a Traditional IRA if you made pre-tax contributions to an IRA before law school, or you changed jobs and rolled a previous 401(k) balance to a Traditional IRA.

If you do have pre-tax money in an IRA, decide if you want to pay the tax bill on the conversion today (if so, jump to step 2).

If you have a higher income, you probably don’t want this money taxed at your current marginal rate and would prefer to keep it pre-tax so you can withdraw it in retirement later at what’s likely to be a lower effective tax rate.

Assuming you don’t want it taxed, you need to remove the pre-tax money. This is because the IRS won’t let you just convert the non-deductible traditional IRA portion of your IRA. You must convert both the non-deductible portion and the pre-tax money, pro rata, when converting to a Roth IRA. If you’re not careful and skip this step, you’ll end up having to pay taxes on the pro rata portion of the pre-tax money since you’re converting it from pre-tax to after-tax.

By December 31st of the tax year, if you do a Backdoor Roth IRA, you can’t have any pre-tax money in your IRAs (unless you’re planning on paying taxes on any pre-tax money you convert).

You have a few options to remove the pre-tax money in any existing IRAs:

- Pay Taxes Now. As discussed above, you can pay taxes on the conversion today. The pre-tax money will be counted as part of this year’s taxable income.

- Reverse Rollover. The IRS allows you to transfer existing pre-tax money to an employer retirement plan (see IRS Publication 509A). Essentially, you can take all of your pre-tax money and drop it into your work’s 401(k) plan (or something similar). If you have good investment options in your workplace’s 401(k) plan, rolling the money over is a good idea anyway, as you’ll consolidate your pre-tax money in one place. For this, your work’s retirement plan must accept incoming rollovers. Check with your HR department.

- Solo 401(k). If your work’s plan does not accept incoming rollovers, you’ll need to have some self-employment income so you can establish a solo 401(k) plan. You don’t need to make a lot of self-employment income to set this up, just a little money will allow you to set up a Solo 401(k) for yourself, which you can then use to accept the incoming transfer from your traditional IRA.

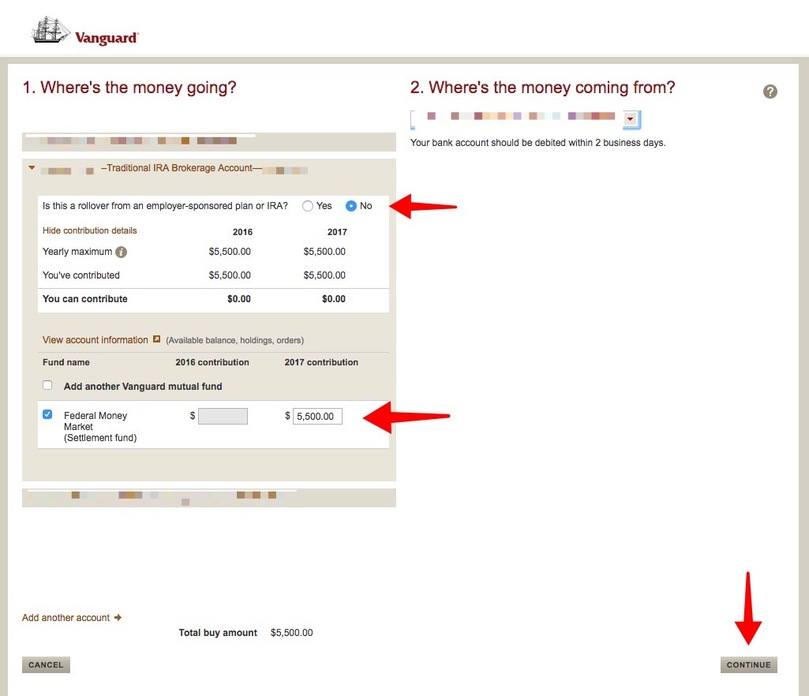

STEP 2) Make a non-deductible contribution to a Traditional IRA

Now that you don’t have any pre-tax money in your IRAs, it’s time to make the non-deductible contribution to a Traditional IRA. Even if your income is “too high,” you can make a non-deductible contribution.

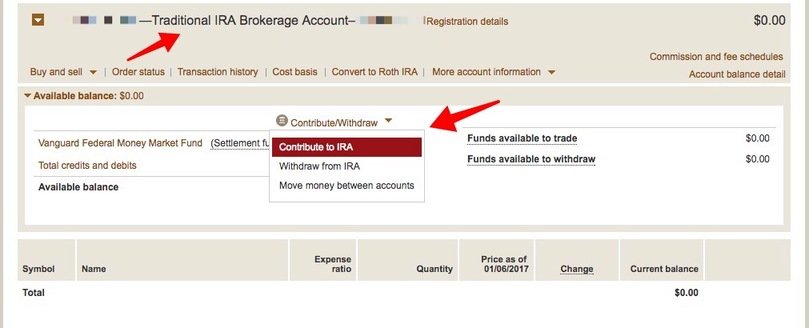

If you don’t have a Traditional IRA account, you’ll need to open one. If you do have one, it should have a zero balance like mine does below.

There are no special steps to make it a “non-deductible” contribution, just make the contribution.

STEP 3) Wait at least one day

Vanguard forces you to wait one day for the IRA funds to settle before you can convert your Traditional IRA to a Roth IRA.

Some people believe you should wait longer and point to the Step Transaction Doctrine as evidence.

In short, the step transaction doctrine is a judicial determination that a series of formally separate steps can be collapsed into a single step for tax purposes. In other words, theoretically, the contribution to the Traditional IRA and subsequent conversion to a Roth IRA could be viewed as a direct contribution to the the Roth IRA, which would be prohibited.

I have never heard of the IRS invoking the step transaction doctrine for a Backdoor Roth IRA contribution. Please let me know if you are aware of it ever being invoked.

I seriously doubt you’re fooling anyone by waiting a week, a month or six months. Regardless, many people would artificially increase the amount of the time between making the “non-deductible” contribution and the subsequent conversion in order to avoid the step transaction doctrine. Me? I’ve always done the conversion the next day.

Vanguard even has a single button you can press to convert the money to a Roth IRA (as you’ll see in the Step 4), so I always assumed the IRS and Congress were fully aware of the “loophole” and would close it if they wanted to.

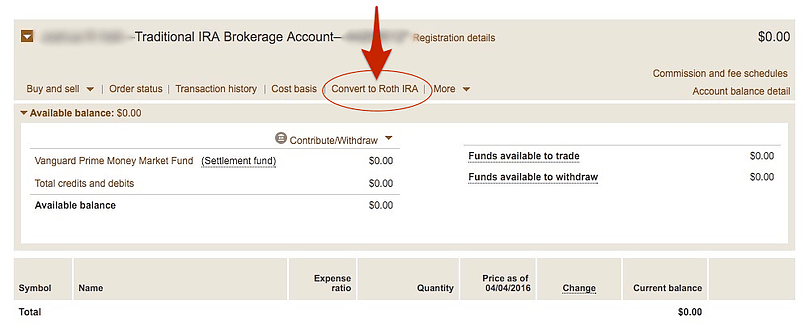

STEP 4) Convert from traditional to Roth

From the Vanguard website, go to your Traditional IRA Brokerage Account and click on “Convert to Roth IRA.”

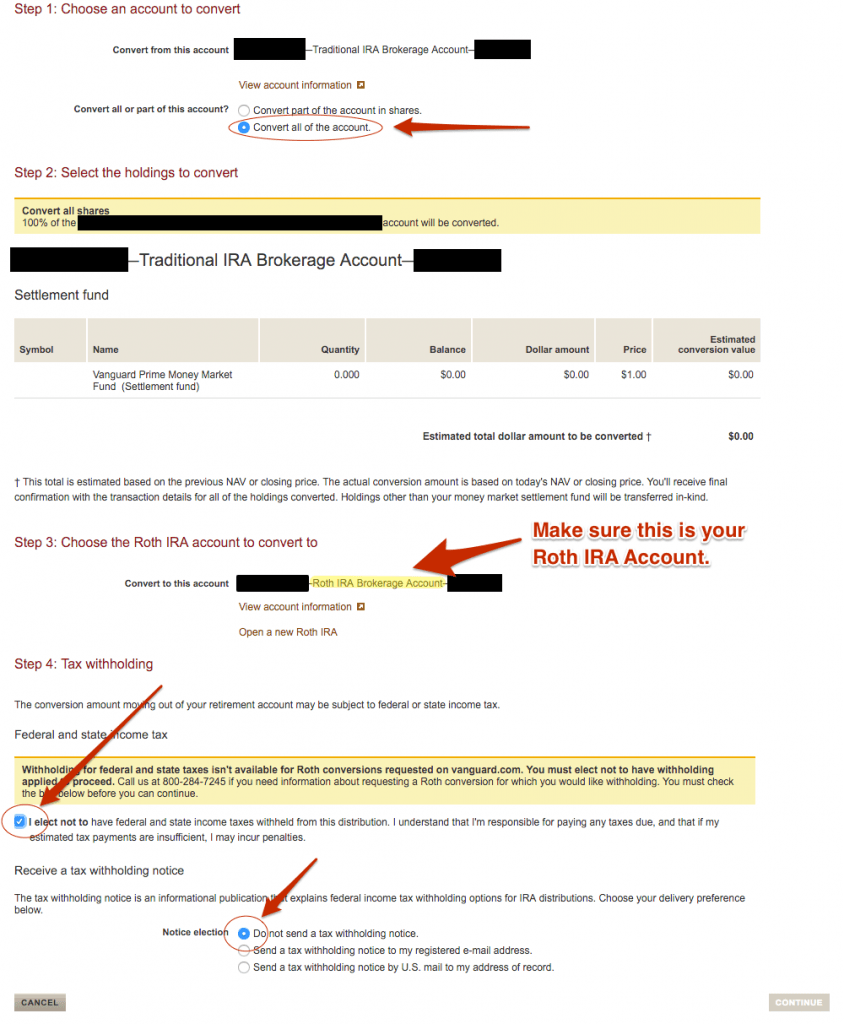

On the conversion page, select that you’d like to convert all of the account into your Roth IRA. If you have an existing Roth IRA, the conversion will roll the funds into your current account. If you need to open a new Roth IRA account, you can do that, too.

At the end of the day, you only need one Roth IRA account, and each year you will roll that year’s contribution into the single account.

After you click on “Continue,” the website will display a scary tax notice. (Update: This year I didn’t see the scary tax notice, so don’t be alarmed if you don’t get it).

Remember, as we discussed earlier, the conversion from a Traditional IRA to a Roth IRA is a taxable event. In your case, the taxes will be zero, so it’s not a problem. Why? Because you made a non-deductible contribution to your Traditional IRA. Income tax would only be due if you are converting a deductible Traditional IRA (i.e. pre-tax money) into a Roth IRA (i.e. post-tax money).

You’re converting post-tax money into post-tax money, so no taxes are due.

After you have converted funds, congratulations! You’ve made a successful “backdoor” contribution to your Roth IRA. You are now free to invest the money in your Roth IRA account.

STEP 5) Report the contribution correctly on your tax return

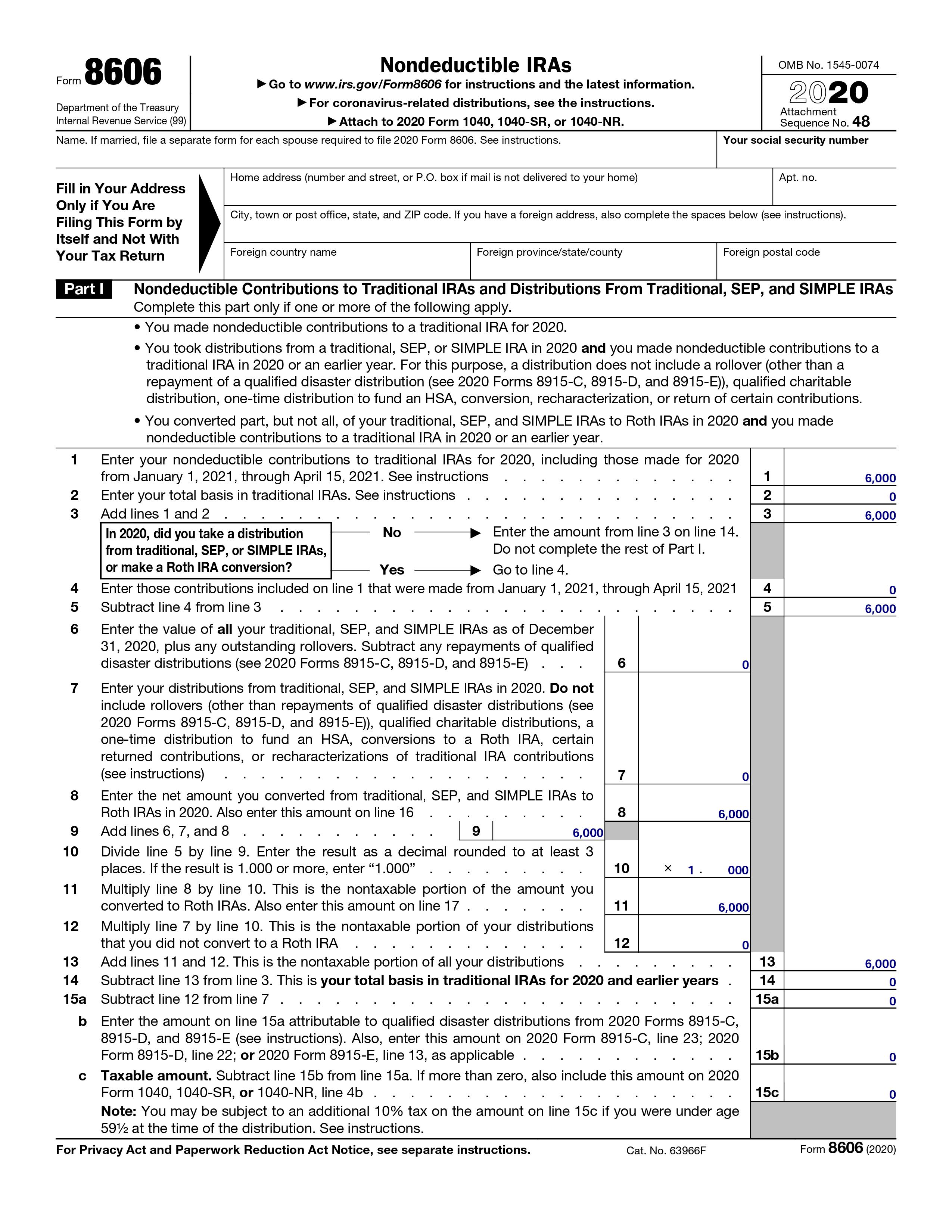

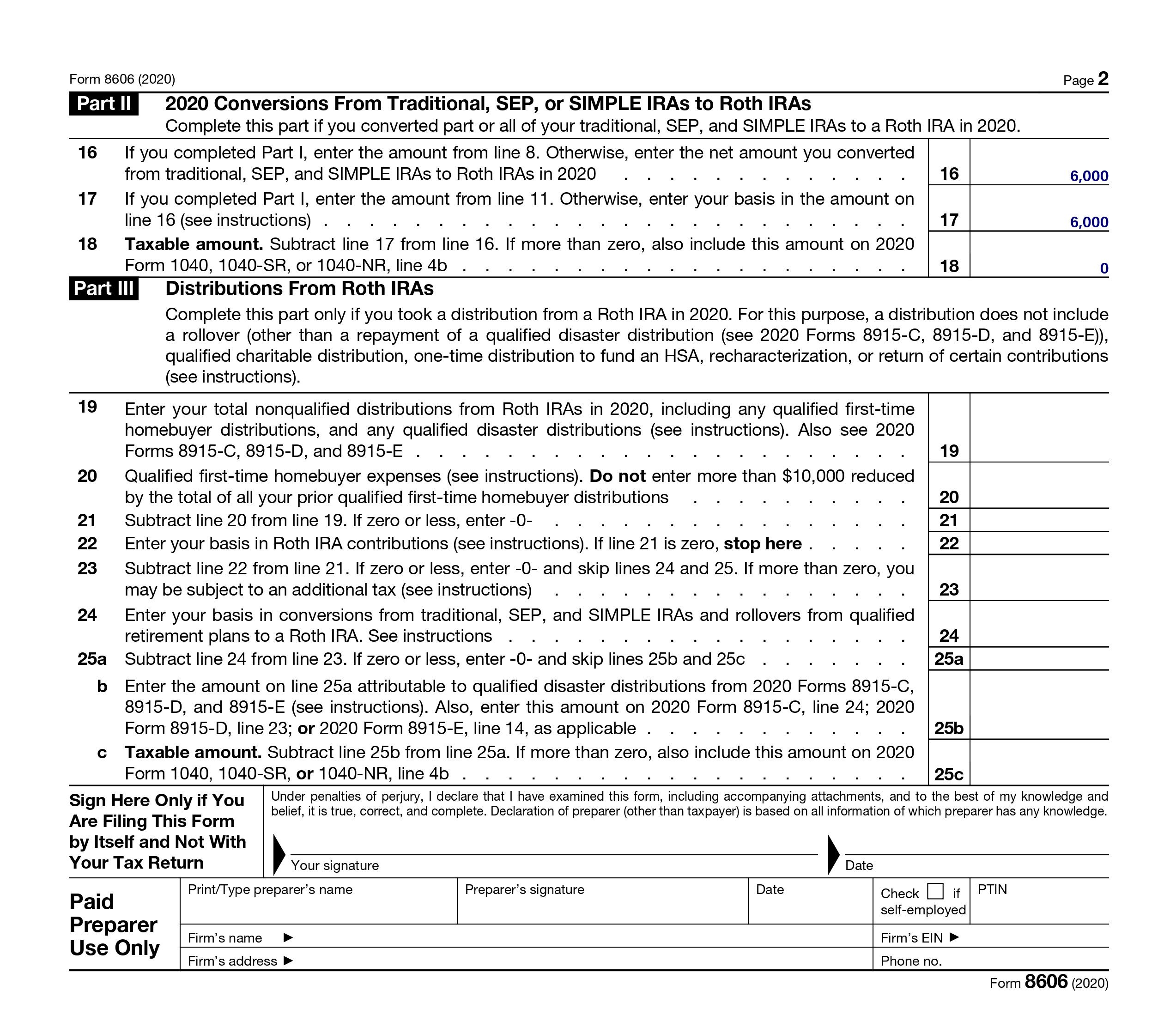

When you report your taxes, make sure you have a correctly completed IRS Form 8606. It’s a short form but there are opportunities to screw it up and confuse the IRS.

Your Form 8606 should look like the image below, unless you’re doing a conversion in a different year from your contribution.

If you’re checking your tax-preparer’s work, focus on lines 2, 14, 15 and 18. All should be a very small amount, likely zero, unless you earned a little interest in the period between making the contribution and doing the conversion. Make sure those lines aren’t large amounts like $6,000.

One interesting aspect of the form is that there’s no place to insert the date you made the conversion (your IRA custodian doesn’t report this either).

Below is how Form 8606 should look:

STEP 6) Repeat next year

Most IRA custodians will keep an account open for a year even if the balance is zero. Therefore, your empty Traditional IRA should be available next year for you to use again when doing your Vanguard Backdoor Roth IRA.

Just remember, you cannot end the taxable year on December 31st with any pre-tax money in your IRA accounts. So, if later this year you leave your employment, you can’t roll your former job’s 401(k) into a Traditional IRA unless you “remove” it again, as described in Step 1.

Will congress close the “backdoor”?

You’re probably also wondering if one day Congress will close the Backdoor Roth IRA. The short answer is no. There have been many discussions about closing the loophole, but as of 2021, it’s still available.

The long answer is that with the Tax Cuts and Jobs Act of 2017, Congress has come as close as ever to officially sanctioning the Roth IRA for high-earners.

The most visible support from Congress for the Backdoor Roth IRA came buried in a conference report released in December 2020 that discusses the TCJA. It looks like we’ve been vindicated, as seen in the following footnotes:

268 Although an individual with AGI exceeding certain limits is not permitted to make a contribution directly to a Roth IRA, the individual can make a contribution to a traditional IRA and convert the traditional IRA to a Roth IRA, as discussed below.

269 Although an individual with AGI exceeding certain limits is not permitted to make a contribution directly to a Roth IRA, the individual can make a contribution to a traditional IRA and convert the traditional IRA to a Roth IRA.

Do these footnotes finally end the speculation as to whether a Backdoor Roth IRA is permitted? I certainly hope so (and several others agree). They’re the clearest guidance we’ve seen that Congress is A-OK with the “backdoor” contributions.

This should comfort a lot of lawyers previously concerned about the step transaction doctrine. Maybe now we need to rename it to the “2-Step Roth IRA” contribution so it will be easier to market!

Some people speculate that Congress is happy to keep the “backdoor” open because each year some people will convert existing pre-tax money in their Traditional IRA to a Roth IRA, thus generating taxable income for the year and raising tax receipts.

Start your backdoor Roth IRA today

Time will tell if the “backdoor” gets closed. Until then, you can take advantage to build a Roth IRA balance even if your income doesn’t allow you to contribute directly.

So, get started with your Backdoor Roth IRA today too boost your personal finances. That’s $12,000 for you and your spouse in a tax-protected account, regardless of your income (or whether your spouse even has earned income).

Have Questions?

What is a Backdoor Roth IRA?

How to do a Backdoor Roth IRA?

Can I do a Backdoor Roth IRA if I have a Traditional IRA?

Can You Still Do a Backdoor Roth IRA in 2021?

Joshua Holt is a former private equity M&A lawyer and the creator of Biglaw Investor. Josh couldn’t find a place where lawyers were talking about money, so he created it himself. He spends 10 minutes a month on Empower keeping track of his money. He’s also maxing out tax-advantaged accounts like 529 Plans to minimize his taxable income.